What are Medicare Supplement Insurance Plans?

Medicare Supplement Insurance Plans (Medigap)

A Medicare Supplement Insurance Plans policy is health insurance sold by private insurance companies to fill gaps in Original Medicare coverage. Supplements can help pay your share of the costs of Medicare‐covered services. Some policies also cover certain benefits Original Medicare doesn’t cover like emergency foreign travel expenses.

If you have Original Medicare and a supplement policy, Medicare will pay its share of the Medicare‐approved amounts for covered health care costs. Then your supplement pays its share. A Medicare Supplement Insurance Plans are different from a Medicare Advantage Plan (like an HMO or PPO) because those plans are an alternative way pay for and receive Medicare benefits – in other words, with Medicare Advantage, those plans are primary. With a Medicare Supplement Insurance Plans, Medicare always pays first, with the supplement acting as secondary insurance.

If you are considering a Medicare Supplement Insurance Plans policy, please keep in mind that they typically have insurance premiums associated with them. These premiums are not paid for by Medicare and must be factored into your monthly or annual insurance budget.

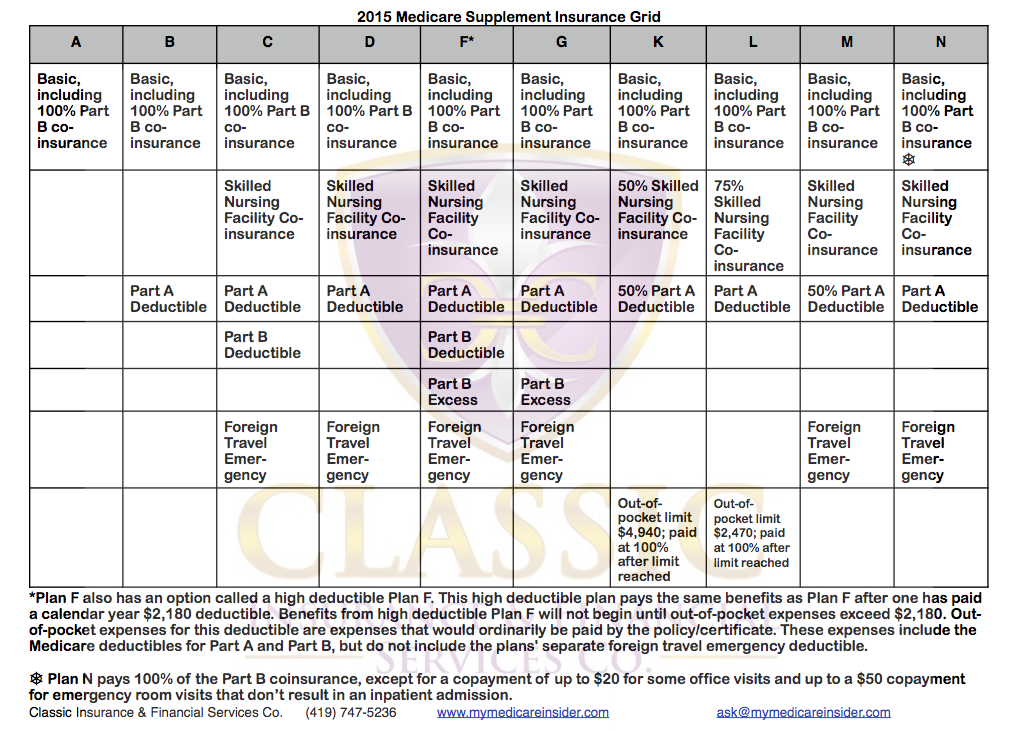

All supplement policies must follow federal and state laws designed to protect you, and policies must be clearly identified as "Medicare Supplement Insurance Plans.” Insurance companies in most states can only sell you a “standardized” Medicare Supplement Insurance Plans policy identified by letters A through N. Each standardized policy must offer the same basic benefits, no matter which insurance company sells it. Cost is usually the only difference between policies with the same letter sold by different insurance companies.

This chart shows what Medicare Supplement Insurance Plans in most states look like. There is a difference in coverage between Medicare Parts A & B and Medicare Supplement Insurance Plans A & B. You can download a copy of this grid here.

Insurance companies that sell supplement policies don’t have to offer every plan. In some cases, an insurance company must sell you the insurance, even if you have health problems.

Here are specific times that you’re guaranteed the right to buy a Medicare Supplement Insurance Plans:

- When you’re in your Open Enrollment Period. For more information about this time, please see open and guaranteed enrollments.

- If you have a guaranteed issue right. This right is limited and very specific. For more information, please see open and guaranteed enrollments.

You may be able to buy a supplement at other times, but the insurance company can deny you coverage based on your health.

To clarify: Medicare Supplement Insurance Plans are NOT part of the Affordable Care Act’s removal of pre-existing condition restrictions! Insurance companies are still allowed to deny you coverage based on poor health unless you are in a guaranteed issue or open enrollment period. In most states, there is no annual guaranteed issue or open enrollment period.

The benefit information provided is a brief summary, not a complete description of benefits. For more information, contact your plan.

Limitations, copayments, and restrictions may apply.

Benefits, formulary, pharmacy network, provider network, premium and/or co-payments/co-insurance may change on January 1 of each year.

Limitations, copayments, and restrictions may apply.

Benefits, formulary, pharmacy network, provider network, premium and/or co-payments/co-insurance may change on January 1 of each year.